Deweloper ma 14 dni na reklamację poznaj swoje prawa!

Deweloper ma 14 dni na reklamację. Dowiedz się, jakie masz prawa, co oznacza brak odpowiedzi i jak działa rękojmia. Sprawdź nasz poradnik!

Klaudia Kucharska

18 października 2025

Deweloper ma 14 dni na reklamację poznaj swoje prawa!

Deweloper ma 14 dni na reklamację. Dowiedz się, jakie masz prawa, co oznacza brak odpowiedzi i jak działa rękojmia. Sprawdź nasz poradnik!

Klaudia Kucharska

18 października 2025

Pszczelna.pl to portal, który łączy pasjonatów rynku nieruchomości. Nasz zespół autorów składa się z ekspertów, którzy dzielą się swoją wiedzą na temat najnowszych trendów, analiz rynkowych oraz praktycznych porad dla kupujących i sprzedających. Znajdziesz tu artykuły, które pomogą Ci podejmować świadome decyzje, niezależnie od tego, czy planujesz zakup nowego mieszkania, czy sprzedaż swojej nieruchomości. Zachęcamy do zgłębiania naszych treści i dołączenia do społeczności, która z pasją podchodzi do tematu nieruchomości!

Dowiedz się, dlaczego deweloperzy ukrywają ceny mieszkań. Poznaj strategie, jak uzyskać informacje i skutecznie negocjować cenę.

Odbiór mieszkania od dewelopera? Poznaj prawa, listę kontrolną i procedurę odbioru. Zabezpiecz swoją inwestycję! Sprawdź nasz przewodnik.

O co zapytać dewelopera przed zakupem mieszkania? Sprawdź nasz przewodnik! Uniknij pułapek, zabezpiecz finanse i wybierz idealną nieruchomość.

Jakie pytania zadać deweloperowi? Skorzystaj z checklisty eksperta! Zapewnij sobie bezpieczny zakup mieszkania i uniknij pułapek. Sprawdź teraz!

Kompleksowy przewodnik po odbiorze mieszkania od dewelopera. Poznaj kroki, prawa i checklistę, by uniknąć błędów. Sprawdź teraz!

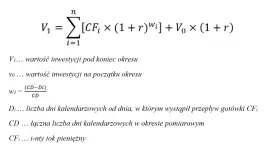

Oblicz realną stopę zwrotu z najmu mieszkania! Dowiedz się, jak uwzględnić wszystkie koszty, wzory ROI i ROE oraz uniknąć błędów. Sprawdź nasz poradnik.

Szukasz mieszkania w Turcji? Sprawdź aktualne ceny wynajmu, koszty (czynsz, aidat, media) i niezbędne formalności dla Polaków. Dowiedz się, jak się przygotować!

Planujesz wynajem mieszkania w Belgii? Sprawdź przewodnik po cenach, kaucjach, mediach i dodatkowych opłatach. Poznaj kluczowe czynniki wpływające na koszt i praktyczne porady.

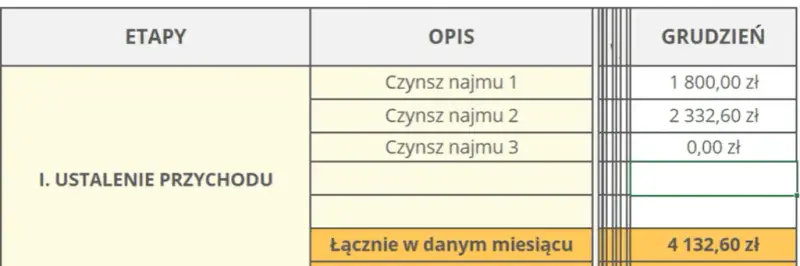

Rozliczasz najem prywatny w 2026? Odkryj, jak płacić ryczałt od przychodów, jakie stawki obowiązują i kiedy złożyć PIT-28. Sprawdź nasz poradnik!